News

As we approach the end of 2024 one knowledge economy sector that has shown significantly increased M&A activity this year is engineering consulting. And whereas previously most M&A in the sector involved the largest strategic acquirers jostling for position in the global top 20, or larger and smaller players turning to organic growth to mitigate pressures on organic initiatives, this year has, in particular, has seen an uptick in sponsor-backed consolidation.

Clearly, engineering consulting covers a broad array of activities, with a corresponding range of project scale, duration, commercial and competitive dynamics. Within this, we are seeing particular interest in engineering know-how relating to the energy efficiency, transportation and infrastructure segments. Moreover, there is growing interest from PE in clean energy and decarbonization, with PE firms increasingly investing in renewable energy; while also supporting their portfolio companies in reducing carbon emissions, with many establishing decarbonization strategies and clear goals for their investments – a factor that is driving additional growth for companies that can support these initiatives.

Artemis has been actively initiating transactions across the engineering consulting space since 2017, but we have seen a notable rise in origination activity in the sector over the last 6-12 months. Founders and investors are now being approached multiple times per month with acquisition inquiries, a significant increase from just a few times per year previously for all but a barbell of a few highly in-demand niche or scale players, demonstrating clear momentum for consolidation in the industry. Historically, these firms often operated as partnerships, allowing individuals to exit by selling their share (or in the case of UK-based businesses setting up EOTs). However, in response to increased demand, we now see seller valuation expectations rising and the range of exit transactions they consider broadening significantly.

The demand comes with qualifications though:

- Niche ecosystems are attracting some of the highest interest. Technically complex sectors like (i) water treatment; (ii) flood design, (iii) transmission and distribution, grid connectivity, and (iv) nuclear engineering are among the most coveted assets and capabilities due to the high degree of specialisation required to secure and excel in high-value projects for the most demanding clients.

- Cross-sector expertise is driving differentiation. Clients now demand holistic solutions that integrate strategic planning, design innovation, and efficient project delivery.

- Regulatory compliance and risk management are in focus. Regulatory compliance and risk management have become increasingly critical in the transport and critical infrastructure sector, particularly in the realm of dispute resolution and claims advisory. The landscape is evolving rapidly, driven by new regulations around sustainability and data privacy. As governments worldwide implement stricter environmental standards and data protection laws (such as GDPR in Europe), companies in the infrastructure space face a complex web of compliance requirements. This complexity often leads to disputes between project stakeholders, contractors, and regulatory bodies. Consultancies specializing in dispute resolution and claims advisory are seeing a surge in demand as they help navigate these challenges.

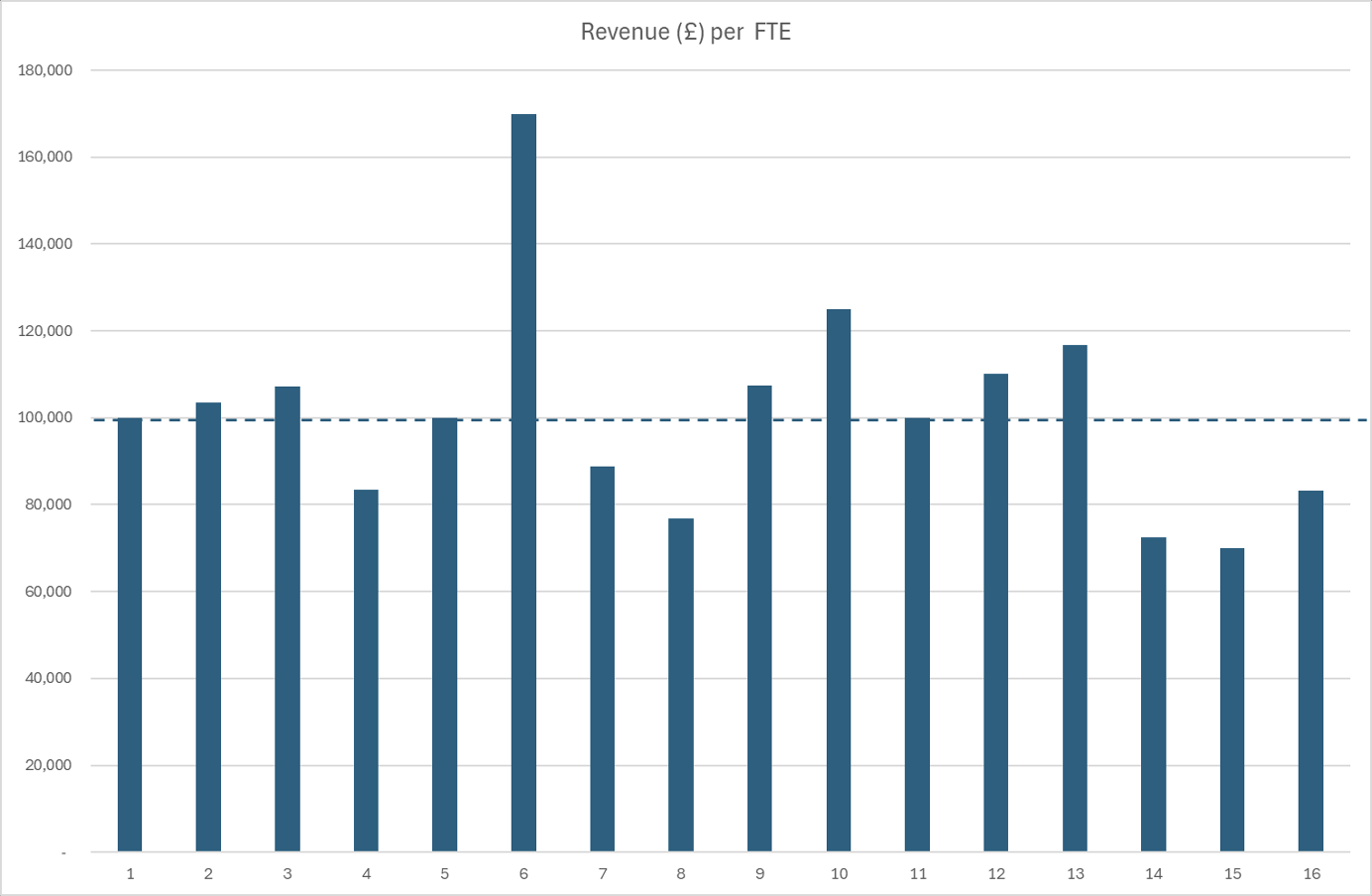

- Best in class Revenue to FTEs. Average revenue per FTE remains around £102k; top quartile is £110k; while industry leaders are generating £150k per FTE or more.

- Focusing on Markets with Strong Policy and Funding Foundations. Markets with robust policy and funding environments continue to attract significant interest. The private sector, particularly in mobility, energy, and resources, offers considerable growth potential as companies navigate decarbonization, electrification, and infrastructure renewal. Public-private partnerships in these sectors are increasingly vital, and firms that can align their expertise with these funding streams will find ample opportunities to deliver impactful projects.

- Improved export model. Savvy acquirers with well-established platforms are leveraging newly acquired talent by redeploying resources from markets experiencing investment cycle pressures (e.g., UK rail) to high-growth regions such as the Middle East, Asia, and North America. This strategy not only ensures immediate utilization but also positions the workforce for a resurgence in domestic demand.

Whilst this is not the first wave of consolidation in the engineering space it does appear to be occurring at a notably faster pace than previously seen – most likely driven by the rising number of PE-backed platforms responding to substantial government funding programmes. Similar to how private equity has strategically invested in software assets through technology service firms, private capital is now shifting focus to the service layer surrounding the rapidly growing real estate and infrastructure sectors, aiming to achieve more attractive risk-reward profiles. And according to that comparison, this trend has a number of years left to run.

Smart Sourcing.

Proprietary Transactions.

Delivering results from investment strategy to close.